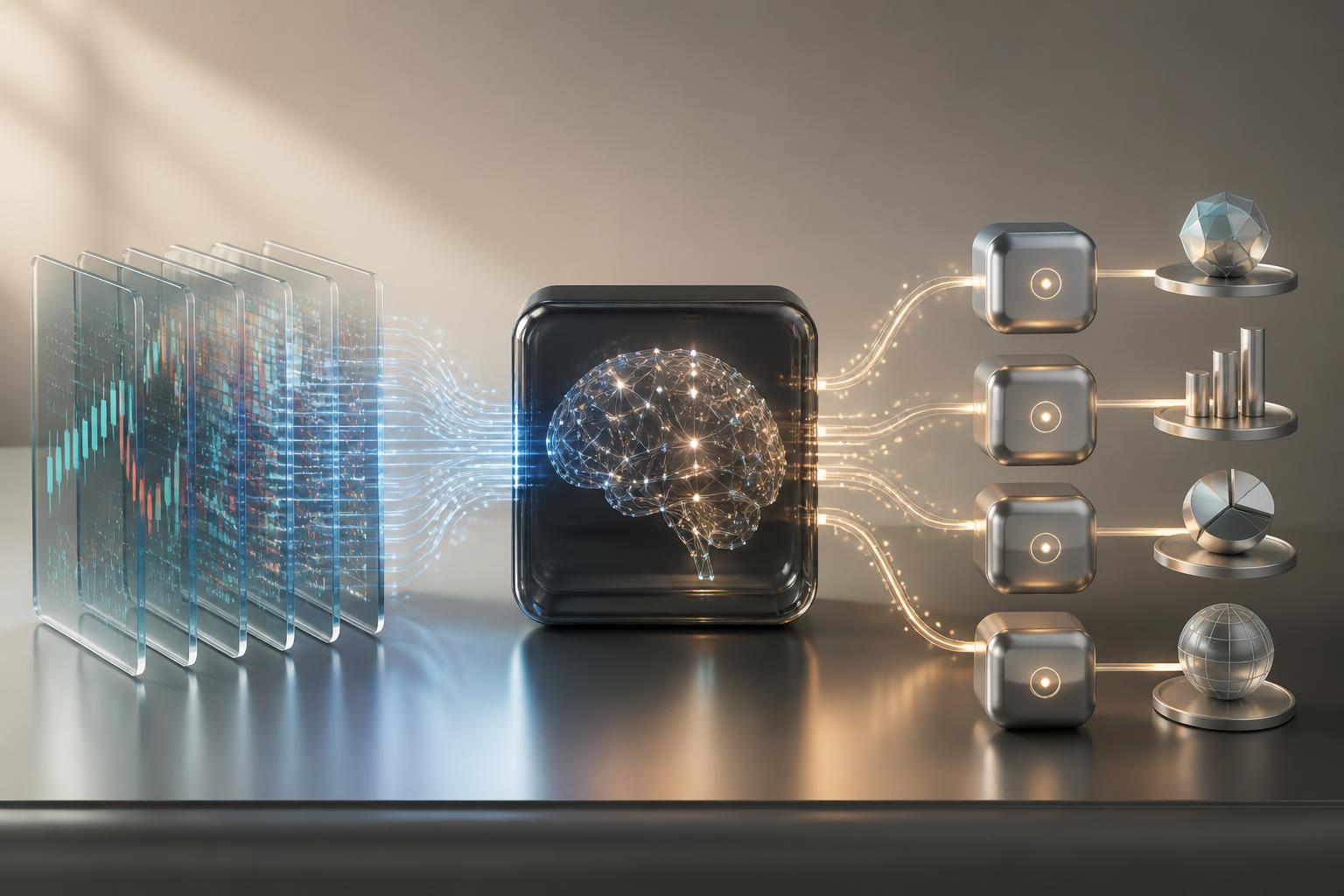

An AI trading model with an API is a system that pulls market data programmatically, turns that data into features, produces a trading signal, and sends simulated or live orders through a brokerage API. The practical way to set one up is to separate the stack into four parts: data, model, execution, and controls.

This is an educational guide, not investment advice. The goal is not to promise profits. The goal is to show how to build a trading workflow that can be tested, paper traded, monitored, and shut down safely when conditions change.

Start with the stack, not the model

Most first-time builders focus on the model too early. In practice, the hardest part is usually not the prediction algorithm. It is choosing the right API setup, defining the target correctly, and building enough controls around execution.

The core parts of an AI trading setup

| Layer | What it does | What can break |

|---|---|---|

| Market-data API | Delivers historical and live bars, quotes, trades, and reference data | Missing fields, delayed feeds, timezone mistakes, bad symbol mapping |

| Brokerage API | Places, modifies, and cancels orders and returns account and fill status | Rejected orders, partial fills, wrong order type, live-money mistakes |

| Model layer | Turns features into a forecast, score, or position suggestion | Overfitting, label leakage, unstable signals |

| Control layer | Applies limits, kill switches, logging, and monitoring | Runaway exposure, stale data, silent failures |

You can use one provider for multiple layers or split the stack. For example, one provider may supply both brokerage and market data, while another setup may use a specialist data API plus a separate broker for execution. The best choice depends on what you are trading, how much market coverage you need, and whether you are still in paper-trading mode.

Choose a brokerage API and a market-data API separately

A brokerage API is for account access and order execution. A market-data API is for prices, bars, quotes, trades, and sometimes news or reference data. Some platforms do both, but you should still evaluate them as separate jobs.

- Brokerage API checklist: paper trading, order types, account endpoints, fill events, position data, rate limits, supported assets, and clear documentation.

- Market-data API checklist: historical depth, live feed type, coverage by asset class, timestamp quality, corporate-action handling, and websocket support for live updates.

- Operational checklist: SDK quality, auth flow, sandbox or paper environment, status page, and how easy it is to separate paper from live credentials.

If you are just starting, optimize for a clean paper-trading environment and reliable historical access before you optimize for speed. A model that cannot survive a controlled simulation should not be wired to live order execution.

Collect data that matches the decision you want the model to make

Before you collect anything, define the exact decision. Are you predicting the next 5-minute direction, ranking a basket for daily rebalancing, or deciding whether to enter only when volatility and liquidity conditions line up? Your target decides the data you need.

Pick a narrow first use case

A good first project is small and observable. For example:

- Predict whether a liquid stock will close above or below its current price over the next 15 minutes.

- Classify whether the next bar move is large enough to overcome estimated fees and slippage.

- Rank a small universe of liquid symbols once per day instead of trying to predict every tick.

A bad first project is broad, vague, and hard to validate, such as “trade the whole market with deep learning.” Narrow the asset universe, the timeframe, and the action space.

Build the raw data pipeline

Your dataset usually needs at least these columns:

- Timestamp in one consistent timezone

- Open, high, low, close, volume

- Corporate-action adjustments when relevant

- Bid and ask or spread data if execution quality matters

- Session information such as pre-market, regular market, and after-hours

Store raw data separately from feature tables. That makes it easier to rebuild features later when you discover a bug or want to try a new labeling rule.

Design features from market behavior, not hype

Feature design should describe price behavior, liquidity, or regime. Useful starter features often include:

- Short and medium rolling returns

- Rolling volatility and range compression

- Volume spikes relative to a moving average

- Distance from VWAP or other reference levels

- Time-of-day and session features

- Spread, quote imbalance, or trade intensity when available

Keep features simple enough that you can explain why each one might matter. If you cannot explain the link between a feature and a trading decision, it usually does not belong in version one.

Choose the lightest model that can answer the question

You do not need the most complex model first. In many trading projects, weak labels, poor validation, or transaction-cost blindness cause more damage than an underpowered algorithm.

Start with baselines before advanced models

Build these in order:

- Naive baseline: always flat, always long during a session, or simple momentum/mean-reversion rules.

- Linear or tree baseline: logistic regression, linear regression, random forest, or gradient boosting.

- More complex models only if justified: sequence models, deep learning, or reinforcement learning after the simpler versions prove there is signal worth modeling.

If a simple baseline cannot outperform a trivial rule after realistic costs, a more complex model usually does not fix the core problem.

Match the model to the output

Common choices include:

- Classification: buy, sell, or do nothing

- Regression: expected return over a fixed horizon

- Ranking: choose the best symbols from a small candidate set

For many builders, classification or ranking is easier to operationalize than predicting an exact future price.

Avoid the validation mistakes that ruin trading models

Three mistakes are especially common:

- Look-ahead bias: using information that was not available at the decision time

- Leakage through preprocessing: fitting scalers or transforms on future data

- Random train-test splits: breaking time order and making results look better than live reality

Use time-based splits, walk-forward testing, and a strict out-of-sample period. Markets change, so the model has to survive different regimes instead of one lucky window.

Backtest first, then paper trade in real time

Backtesting tells you whether the idea survives history. Paper trading tells you whether the live system behaves the way the backtest assumed. You need both.

How to run a useful backtest

A backtest should simulate the exact rules your live system will use:

- Signal generation timing

- Order type and entry rules

- Position sizing

- Stops or exit conditions

- Commissions, fees, spread, and slippage assumptions

- Market hours and trading halts

Do not celebrate a backtest that ignores friction. A strategy that looks profitable before slippage and fees may disappear after you model execution realistically.

What paper trading should prove

Paper trading is not just a fake-P&L exercise. It should answer operational questions:

- Does the data arrive on time?

- Does the feature pipeline update correctly?

- Do orders get submitted only when rules allow them?

- Do fills, partial fills, and rejections update the portfolio state correctly?

- Can you restart the process without losing track of positions?

Paper trading should run long enough to expose boring failures such as clock drift, duplicate orders, reconnect issues, and stale websocket data.

Add execution guardrails before any live order goes out

A trading model should not have direct freedom to place unlimited orders. The model should suggest an action, and the execution layer should decide whether that action is allowed.

Minimum guardrails for version one

- Position limit: maximum shares, contracts, or notional per symbol

- Daily loss cap: stop trading after a defined drawdown threshold

- Open-order cap: prevent accidental order floods

- Liquidity filter: trade only symbols with acceptable spread and volume

- Session filter: restrict trading to allowed market hours

- Stale-data check: block trading if the latest quote or bar is too old

- Kill switch: one command to cancel orders and stop the strategy

Also decide which order types the system is allowed to use. Many early systems should prefer bounded, understandable behavior over maximum speed. If you cannot explain how a given order type behaves in thin or fast markets, do not automate it yet.

Separate signal logic from execution logic

This is one of the most important design decisions. The signal layer can say, “I want 20 percent of the current allowed position.” The execution layer then checks limits, rounds sizes, chooses the allowed order type, and decides whether the order should be sent at all. That separation makes audits, testing, and shutdowns much easier.

Monitor the system like software, not like a black box

Once the model runs continuously, you are operating a production system. P&L matters, but it is a lagging metric. You also need operational monitoring.

What to monitor continuously

- Data latency and missing bars

- Feature freshness and null rates

- Prediction distribution and confidence drift

- Order rejects, cancels, and partial fills

- Position reconciliation between your system and the broker

- Runtime errors, retries, and reconnect frequency

- Daily exposure by symbol, strategy, and account

Set alerts for conditions that mean the model may be acting on bad inputs. A mediocre model with strong monitoring is often safer than a strong model with no observability.

Review model drift on a schedule

Even if the code is stable, the market regime may not be. Review feature importance, confusion matrices or hit rates, turnover, average holding time, and the gap between expected and realized execution cost. If those move materially, the model may need retraining, tighter filters, or retirement.

Protect API keys and separate environments

API keys are part of the trading system, not a setup detail. Treat them like production secrets.

- Never hard-code keys in source files or notebooks you share

- Keep paper and live credentials separate

- Use environment variables or a secret manager

- Rotate keys when people, machines, or vendors change

- Restrict who can access live credentials

- Log key usage and failed authentication attempts

- Keep model prompts, chat tools, and debugging transcripts free of secrets

One simple rule helps a lot: a development machine should not quietly have access to live trading keys by default. Make live access explicit, reviewed, and reversible.

A practical first implementation path

- Pick one asset class and one small universe of liquid symbols.

- Choose a market-data API and a brokerage API with paper trading.

- Define one decision, one horizon, and one target variable.

- Collect and store clean historical data.

- Build a trivial baseline and then a simple ML baseline.

- Backtest with fees, slippage, and session rules included.

- Run the same logic in paper trading for multiple weeks.

- Add limits, stale-data checks, and a kill switch.

- Set up monitoring for data, predictions, orders, and positions.

- Only then consider a tightly constrained live rollout.

If you follow that order, you will learn faster and lose less time than teams that start with a complex model and no execution discipline.

Common mistakes to avoid

- Using a delayed or incomplete feed without realizing it

- Training on adjusted data and trading on unadjusted live inputs

- Ignoring spread and slippage in backtests

- Letting the model place orders without a separate control layer

- Optimizing for backtest performance instead of operational reliability

- Putting live keys on laptops, in notebooks, or in chat logs

- Believing that “AI” removes the need for market structure knowledge

The winning habit is skepticism. Treat every attractive result as something that still needs to survive cleaner data, stricter assumptions, and a longer paper-trading period.

Final takeaway

Setting up an AI trading model with an API is not mainly a modeling challenge. It is a systems challenge. If you choose clean APIs, define a narrow target, start with simple models, backtest honestly, paper trade patiently, and build strong guardrails, you will have something useful to evaluate. If you skip those steps, the model quality usually does not matter because the surrounding system is not trustworthy enough to run.